Agricultural Credit Marketplace

Principal Product Designer · Traive · 2024

Traive was an AI-driven agricultural credit platform operating in Brazil, where many agricultural producers lack access to formal credit because traditional lenders can't adequately model farming risk.

My role was to define the company's next strategic product from concept to development-ready: a two-sided marketplace connecting mainstream financial institutions with agribusinesses holding farm receivables, with Traive's proprietary AI underwriting the risk on both sides.

Principal Product Designer on a net-new product with no predecessor and no existing model to adapt.

I owned end-to-end discovery and delivery in a remote, multilingual environment — research conducted across Brazilian Portuguese and English, with users ranging from rural agribusiness operators to institutional fund managers.

My Role

The existing process for buying and selling agricultural receivables through Traive was a multi-party chain running on a fixed weekly cadence with almost no automation and no visibility for any of the participants outside of Traive's own CS team, which functioned as a human relay between everyone.

The concept for the marketplace had existed in the company's vision since founding years prior. Defining what it actually was — structurally, operationally, at the level of who does what and when — and then bringing that to life on screen, was the work.

The Problem

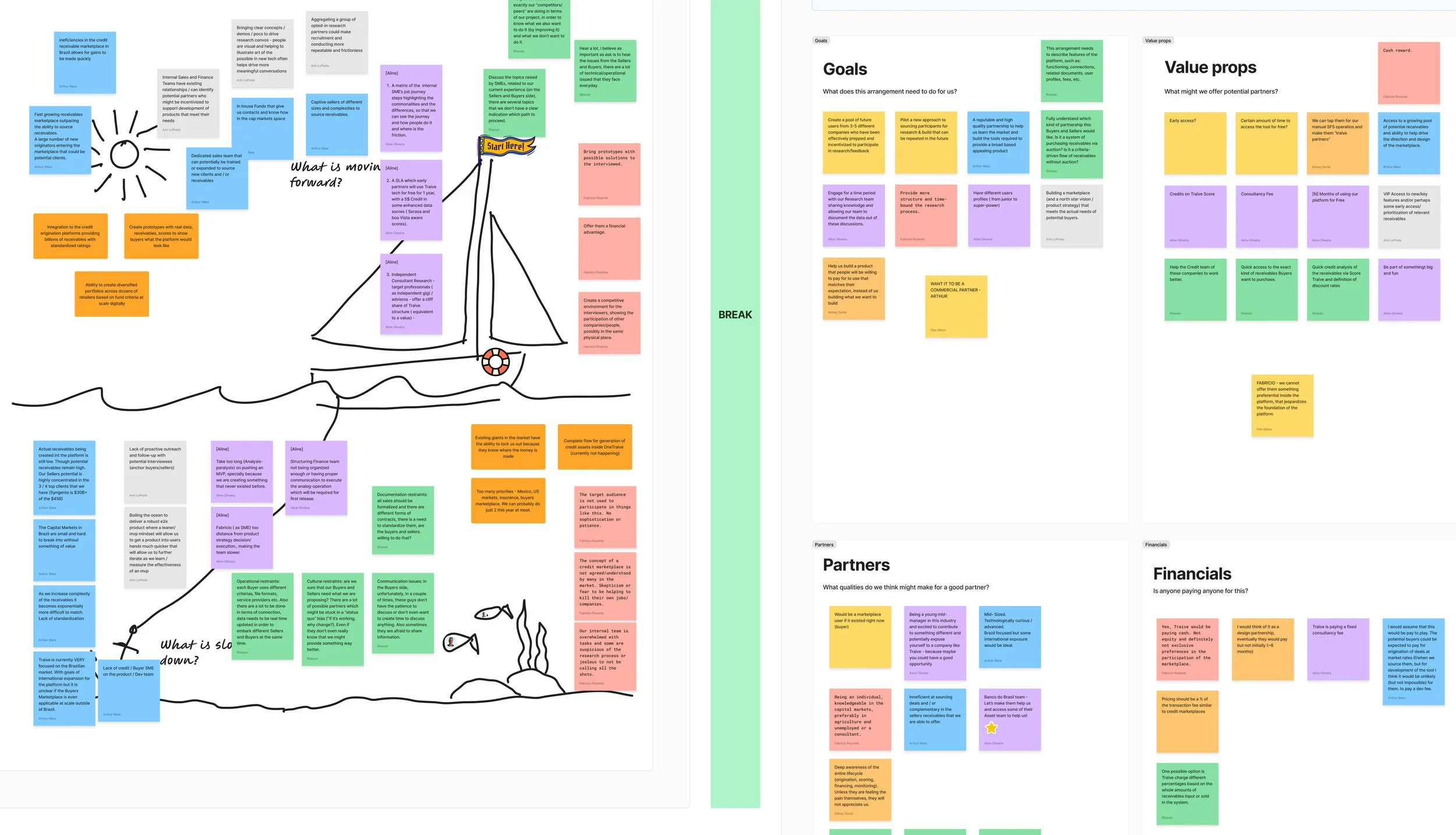

The Research

User interviews with financial institution stakeholders and agribusiness operators, outcomes from previous guerrilla research with producers in the field, all brought together in a series of cross-functional workshops with the internal team and trusted external SMEs.

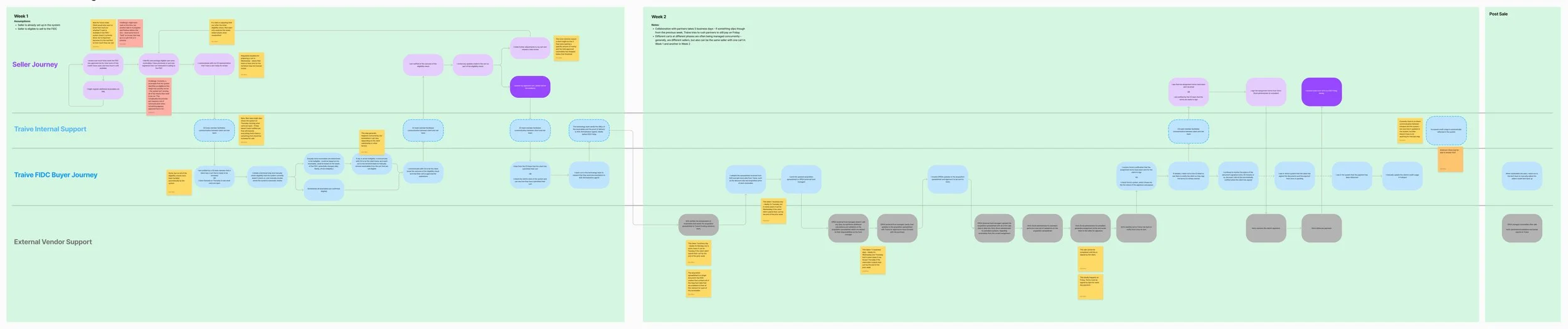

The most critical document I synthesized from these was a detailed service blueprint mapping the current transaction process across four swim lanes: Seller Journey, Traive Internal Support, FIDC Buyer Journey, and External Vendor Support. Even our very engaged founder and CEO had never quite seen and understood the complexity of the current state in such clear detail.

What it surfaced

Though digitized, the entire system was opaque to its participants until it was manually updated.

Sellers had no visibility into how much capital the fund had available — the real constraint on what they could sell. Buyers didn’t know what sellers had available until they were already assembling the cart. The risk team manually re-checked eligibility the system hadn't fully validated. Every status update to every party flowed through CS.

Every major design decision in the marketplace traces back to something specific highlighted by the research and service blueprint.

The Strategy

Stakeholder alignment sessions with the CEO and product triad translated the research into a product architecture: two distinct experiences — seller and buyer — connected by Traive's AI score at every decision point, with tiered access to information based purely on the relationship between a buyer and seller, no middleman.

-

A core value proposition for this marketplace was to alleviate the discoverability friction in what had always been a very relationship-based marketplace. Trusted personal connections were the only way to reduce time and effort spent finding each other, let alone figuring out if there was a mutually beneficial financial opportunity. You can imagine this marketplace impacting Brazilian agribusiness similarly to Etsy’s impact on artisan makers.

The Solution

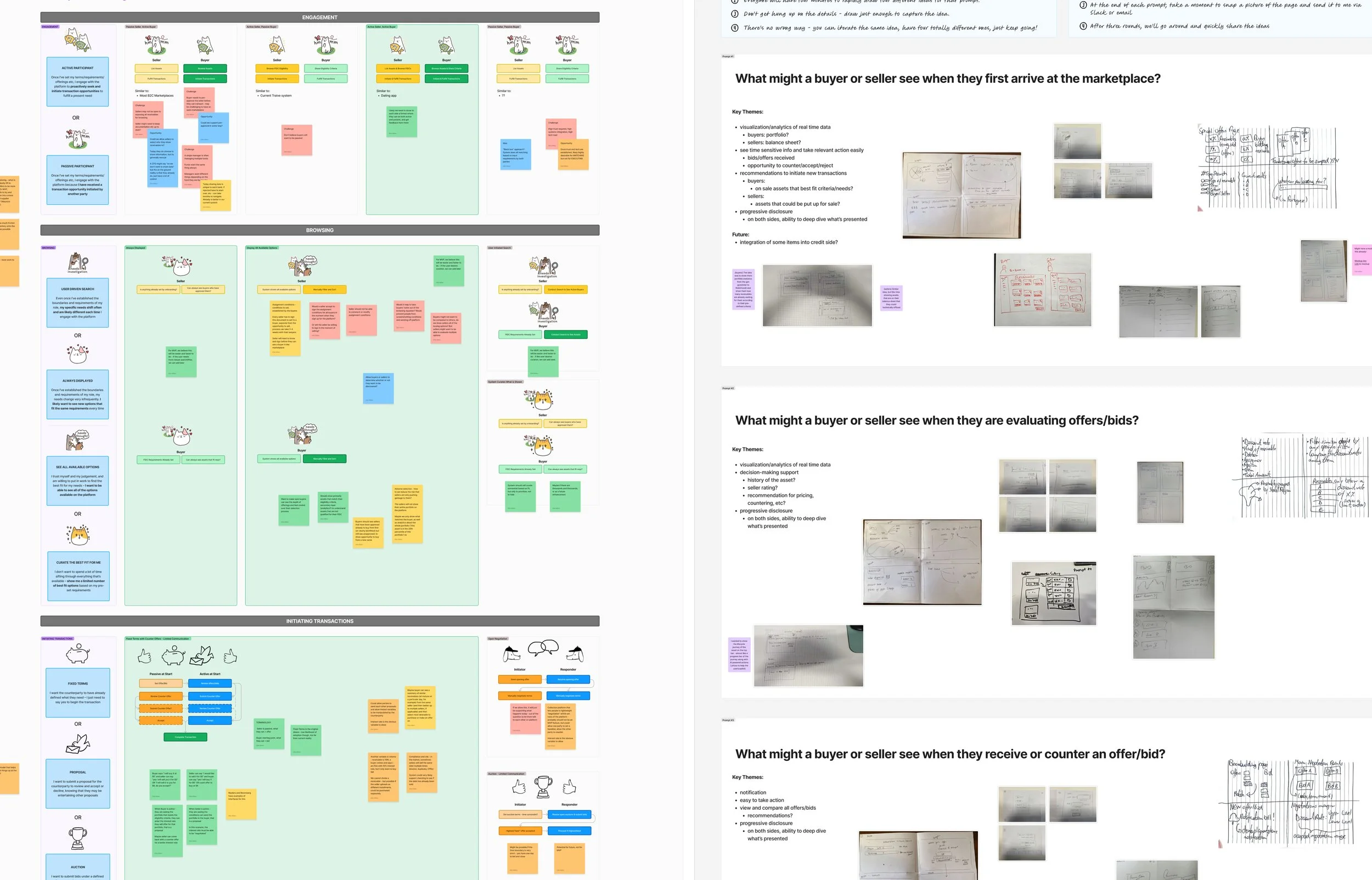

SELLER SIDE

The dashboard serves as home base and surfaces credit limit utilization — total, used, and available — and a recent activity feed for new and in-progress deals, giving sellers the fund cash availability and up-to-date status visibility that the current process entirely lacked.

Sellers manage incoming offers from buyers as carts — bundles of receivables a buyer has assembled for purchase. Status tags give an at-a-glance read.

A warning banner flags duplicate receivables appearing across multiple competing buyer carts, since a receivable can only be sold once. The red clock signals an offer that’s nearing its expiration date, so they don’t miss something time sensitive.

The comparison view places buyer offers side by side. At the receivable level, color-coded AI scores, discount rates, disbursement dates help guide decision making, and replaces a process that previously required a CS representative to walk them through competing offers verbally.

Once a cart is accepted, a seven-step progress tracker gives sellers life changing visibility into a process that previously involved multiple parties, a fuzzy week-long timeline, and no knowledge of when the transaction would complete.

The Result

A platform that gives sellers unparalleled ease of discovery, receivables management, offers comparison, and industry-reshaping transparency into the sales process.

The Solution

BUYER SIDE

Buyer access to seller information is tiered.

A buyer sees an unvetted seller only as "Vendedor #XXXXXX" — top-level financials visible, identity withheld, one action available: request access.

Provisional approval by the seller reveals their identity and portfolio for the buyer’s evaluation and approval process.

Full approval unlocks relationship data, cart creation and management, and financial statements – normally all maintained manually, now centralized and automatically updated.

A buyer viewing a fully approved seller can also access a full portfolio evaluation, including the aggregate risk score distribution, a geographic and crop exposure breakdown, a maturity distribution chart, and a filterable receivables table.

Filters by eligibility, score band, crop type, maturity window, and credit status let buyers build a position thesis before committing to individual purchases.

Selecting any receivable opens a detail panel: AI score, suggested discount rate, acquisition price, type, guarantee status, maturity, and supporting documentation. Everything needed to make a credit decision without leaving the portfolio view.

Every integrated receivable traces back to a centralized producer profile.

Traive's AI-powered score surfaces most prominently here as a composite number with a confidence interval, anchored against a familiar credit-rating equivalent — a B+, in this case — so buyers could read the proprietary score in language they already used.

Below it, a breakdown across five dimensions: Agronomic, Market, Financial, Behavioral, and Sustainability & Compliance. Each draws on different signals — satellite imagery, climate data, soil type, cultivation practices, commodity prices, payment history — and each is drillable to its underlying data. Prominent on the page, never the gate.

Buyers could build their own thesis from the data while learning to trust our analysis at their own pace.

The Result

A platform that takes the most manual, time consuming parts of investing in agribusiness – vetting sellers and gathering the data to evaluate the risk of acquiring their receivables – down to nearly zero, while keeping buyers in the drivers seat of their analysis.

Outcomes

The work established a viable product definition for a first-of-its-kind agricultural receivables marketplace — development-ready in under six months, with a leadership team aligned on what they were building. Unfortunately, Traive ceased operations shortly after launching the marketplace for unrelated reasons.

The success of this effort was in bringing this incredibly complex, outcome-driven strategic pillar out of the founders’ heads and onto the screen in just six months.